The global economy rests on a delicate balance of trust and investment. At the heart of this system lies the US Treasury market. However, a hypothetical scenario exists that economists often describe as a financial nuclear bomb.

This scenario is no longer just a mathematical exercise but a potential geopolitical tool. If the United States, under the Trump administration, were to take the unprecedented step of militarily attacking and conquering Greenland, Europe could be forced to respond with its most powerful economic weapon.

Imagine if every European entity (including governments, central banks, and private investors) decided to simultaneously dump their combined holdings of approximately $3.6 trillion in US Treasury bonds as a direct consequence of such an invasion.

The Chain Reaction

If this “horror scenario” were to unfold, here is the step by step breakdown of what would likely happen:

A Crash in Bond Prices: A sudden flood of $3.6 trillion worth of bonds onto the market would cause their value to plummet instantly due to the massive oversupply.

Skyrocketing Interest Rates: As bond prices crash, the yields (interest rates) would spike to extreme levels. This would make US government debt significantly more expensive to maintain.

The Dollar in Freefall: To exit these investments, European investors would need to sell their US dollars. This massive sell-off would likely cause the value of the US dollar to collapse against the Euro.

Global Market Chaos: Because the US Treasury bond is the benchmark for the global financial system, its collapse would trigger a domino effect. Stock markets would likely tank, and borrowing costs worldwide would become unaffordable overnight.

While the military conquest of Greenland remains a shocking concept, this financial “nuclear option” highlights that Europe’s choice to divest could be the ultimate check on such a massive shift in international relations.

If you had followed the economic forecasts at the start of 2025, you’d have been tempted to hide under the stairs with a blanket and a survival kit. The narrative was clear: the return of Donald Trump and his aggressive tariff regime would signal the end of the global economy as we knew it.

Experts predicted the largest trade shock in history, with some warning that a global recession was almost a mathematical certainty.

Yet, as we reach the end of the year, the wreckage is surprisingly hard to find. The world is still turning. While growth has slowed, the much feared recession hasn’t materialized. Global trade has undergone massive shifts behind the scenes, but it has neither halted nor collapsed. This raises a fundamental question: are our economic models broken, or has the global trading system proven far more resilient than anyone dared to hope?

Uncertainty as a Tool

One reason the dire predictions missed the mark is that they took initial announcements at face value. It has since become clear that the “April shock” of sky-high tariff announcements was a deliberate strategy of injecting uncertainty into the market to gain leverage. The goal was always to start high and negotiate down. While journalists and analysts were asking what the direct impact of a 27% tariff would be, the reality on the ground was a moving target. By November, after rounds of intense negotiations, the effective average tariff had dropped to 17%. While this is still significantly higher than the pre-2025 average of 2.5%, it is a far cry from the “total trade war” originally envisioned. Most major economic blocs managed to negotiate their way down, leaving China as the only player facing extreme rates above 40%.

Restraint and Resilience

The second reason we avoided a total meltdown was a surprising display of global self-discipline. The catastrophic scenarios relied on a domino effect of retaliatory tariffs. However, most of the world chose not to strike back in kind. Because the primary burden of a tariff falls on the country imposing it (as a tax on its own importers), the rest of the world avoided much of the pain by simply refusing to escalate. It was a calculated choice of restraint over ego.

Furthermore, global trade proved to be remarkably agile. We often think of international commerce as a slow-moving tanker, but this year showed it can pivot like a speedboat. When routes to the U.S. became too expensive, fleets redirected, and trade intensified within other regions. While exports from Europe to the U.S. have dipped, they haven’t cratered. Meanwhile, global trade in goods actually rose by over 6% this year. The old adage that “when America sneezes, the world catches a cold” no longer seems to hold true; we are moving toward a more balanced, less U.S. centric global economy.

The Hidden Toll

Does this mean the tariffs were a victimless policy? Far from it. While the “doomsday” didn’t happen, a slow erosion is visible beneath the surface.

The pain is currently being masked by corporate buffers. To avoid losing market share, exporters are slightly lowering their prices, while U.S. importers are eating into their own profit margins or cutting costs elsewhere rather than passing the full cost to the consumer immediately. Additionally, many companies stockpiled goods before the tariffs took effect, allowing them to sell older, cheaper inventory throughout the year.

However, these buffers are not infinite. Inflation in the U.S., which had been trending downward before the inauguration, has begun to creep back up. The promised manufacturing boom has yet to materialize, and job growth has stalled. Perhaps most tellingly, the tariff revenue is nowhere near enough to replace income tax, as was once claimed.

The real test will come in the next six months. As stockpiles empty and profit margins hit rock bottom, businesses will be forced to pass costs onto the public. This won’t just affect imported goods, but will trickle down into services like healthcare and hospitality. The economic “hell and damnation” didn’t arrive with a bang in early 2025, but for the American consumer, it may yet arrive with a whimper just in time for the midterm elections.

The European Union is working on a second “Chips Act” to strengthen its own, independent semiconductor industry. Not only for cutting-edge AI chips, but also for basic, low-cost chips used in everyday products like cars.

The message from Brussels is clear: Europe must become less dependent on foreign technology and more resilient in times of geopolitical crisis. But how realistic is that ambition?

At a semiconductor conference in Munich, European Commission official Pierre Chastanet admitted that Europe was caught off guard by the recent Nexperia crisis. The company, now owned by Chinese investors, became the center of a diplomatic conflict after Dutch government intervention. The result was risks to Europe’s automotive supply chain and the threat of yet another chip shortage. For Chastanet, it was a painful reminder that Europe’s chip supply is far less secure than it would like it to be.

From the First Chips Act to a Second Wave

The first European Chips Act, launched in 2022, marked a turning point in EU industrial policy. A total of 43 billion euros was mobilized, mainly through national governments and the EU budget, to stimulate semiconductor production in Europe. This helped attract major investments, including the ESMC chip plant in Dresden, a joint venture between TSMC, NXP, Infineon and Bosch, which is expected to start production in 2027. GlobalFoundries is also expanding its presence in Germany and France.

But not everything has gone according to plan. The major Intel investment in Magdeburg has been postponed, and a new plant in Crolles, France, is facing delays. Critics argue that smaller European technology firms still struggle to access high-end production facilities and infrastructure, limiting the emergence of true European chip champions.

Chips Are Geopolitical Power

Semiconductors are more than just technology. They have become a key geopolitical asset. Today, Europe remains heavily dependent on the United States and Taiwan for advanced AI chips. Taiwan, however, sits at the center of growing tensions with China, making Europe’s reliance on Taiwanese production a strategic vulnerability.

Although a planned American law to restrict AI chip exports, known as the AI Diffusion Act, was eventually scrapped by Donald Trump, the dependency remains. Europe cannot afford to entrust its digital future entirely to foreign powers.

Experts argue that chips will be one of the most important geopolitical instruments of the coming decades. The automotive industry, for example, will need increasingly advanced semiconductors for electric vehicles and self-driving technology. Ideally, those chips should come from European factories. Yet production in Europe is expensive, and manufacturers will only invest if there is sufficient demand.

The Missing Link: European System Champions

Europe is not starting from zero. Companies like ASML, for chip equipment, ARM, for chip architecture, and research institutes such as Imec in Belgium and Leti in France form a world-class ecosystem. The EU also holds strong positions in photonic chips and quantum technology.

What Europe lacks, however, are so called system champions, such as Nvidia, Apple or Huawei. These are companies that not only design chips but also shape entire technology ecosystems around them.

Taiwan’s success, experts note, is not based on one-off subsidies, but on long-term government support, tax incentives and continuous investment in the wider technology ecosystem. That is a key lesson the EU would need to embrace.

Practical Obstacles

Beyond strategy and money, practical problems remain. Building a chip factory in Europe takes about twice as long as in Taiwan. Bureaucracy, complex regulation and a shortage of skilled workers are slowing projects down. A single new fabrication plant can require up to a thousand specialized welders, professionals who are currently in short supply across Europe.

Reality Check

The original goal of producing 20 percent of the world’s chips in Europe now looks unrealistic. Out of around 5,000 standard ASML lithography machines worldwide, only 400 are located in Europe. According to ASML representatives, Europe’s chip industry is growing only half as fast as in other parts of the world.

Still, the EU sees no alternative. If it wants to remain economically, technologically and militarily relevant, it must close the massive gaps in its semiconductor industry. The second Chips Act is not just an industrial program. It is a geopolitical necessity.

A neutral analysis of political, ideological, and structural barriers to the Trump administration’s peace proposal.

The peace framework proposed by U.S. President Donald Trump aimed to end hostilities between Israel and Hamas by combining ceasefire measures, economic incentives, and regional mediation. Despite its ambition, the plan underestimates entrenched ideological positions, fragmented Palestinian representation, mediator credibility constraints, and implementation risks—factors that comparative peace-process research identifies as decisive.

1. Ideological incompatibility

Hamas does not recognize Israel’s legitimacy and prioritizes armed resistance; Israel treats Hamas as a terrorist actor to be contained or dismantled. Absent reciprocal legitimacy, negotiations on sovereignty and coexistence lack a viable foundation.

Peace agreements rely on a minimum level of mutual recognition. Without it, negotiations collapse into tactical pauses rather than long-term settlements. Transformative peace requires a shift in legitimacy, not just tactical compromise.

2. Fragmentation of Palestinian representation

The Trump plan largely bypassed the Palestinian Authority (PA), the internationally recognized representative of the Palestinian people. By implicitly engaging with Hamas while marginalizing the PA, the proposal deepens the political split between the West Bank and Gaza. Without internal Palestinian unity, any peace agreement lacks credibility and implementation capacity.

Durable peace agreements depend on unified leadership. As long as the Palestinian Authority and Hamas pursue separate agendas, no framework can represent the Palestinian people as a whole.

3. Misplaced emphasis on economic incentives

The plan’s emphasis on economic growth and infrastructure investment misunderstands the nature of the conflict. The struggle is not primarily about poverty; it is about sovereignty, self-determination, and historical justice. Economic aid cannot substitute for political compromise. Previous attempts to “buy peace” through development funding have failed because they ignored these fundamental issues.

4. Perceived bias of the mediator

The credibility of the United States as a mediator was undermined before negotiations even began. The Trump administration’s decision to move the U.S. embassy to Jerusalem and cut funding to UNRWA was interpreted by Palestinians as clear evidence of pro-Israeli bias. Effective mediation requires both power and perceived impartiality; the U.S. under Trump possessed the former but lacked the latter.

5. Implementation and enforcement challenges

The proposed multi-phase process—ceasefire, disarmament, reconstruction, and administrative reform—faces daunting implementation challenges. The security environment in Gaza remains volatile, and trust between the parties is virtually nonexistent. Without robust monitoring and enforcement mechanisms, compliance with the plan’s provisions would likely erode rapidly.

6. Lack of regional and legal anchoring

Successful peace agreements in the Middle East have historically relied on regional buy-in and international legal legitimacy. The Trump plan’s lack of clarity on Palestinian statehood, refugee rights, and international law left it isolated from both regional actors and global institutions. Without legal grounding and multilateral support, such initiatives struggle to achieve lasting acceptance.

Conclusion

While the Trump peace plan incorporated some pragmatic components—such as reconstruction, governance reform, and regional diplomacy—it neglected the essential political and ideological foundations of peace. Without mutual recognition, unified Palestinian representation, credible mediation, enforceable mechanisms, and a clear legal framework, the proposal remains a symbolic gesture rather than a viable roadmap to peace.

It appears that Hamas is using the deal as a breathing space and an opportunity to retreat with minimal loss of face. Israel is releasing 2,000 prisoners, and Hamas can regroup and strengthen. The leverage they had—the Israeli hostages—is now gone. The question is whether the majority of Palestinians still recognize Hamas’s legitimacy or whether they are weary and ready to hand over governance to the international community, with Israel playing a significant role in that process.

—

References and Further Reading

International Crisis Group — Israel/Palestine analyses

Wat gaan we stemmen op 29 oktober? En waarom wegen de feiten voor veel kiezers minder zwaar dan sentimenten? Voor mij is dat een grote vraag. Zo ingewikkeld zijn de argumenten van radicaal-rechts namelijk niet te weerleggen.

In Nederland hoor je steeds vaker harde geluiden van radicaal-rechtse partijen. Ze beloven simpele oplossingen voor grote problemen: minder immigratie, lagere EU-bijdrage, geen klimaatbeleid, stikstofregels weg en vooral “eigen volk eerst”. Klinkt misschien aantrekkelijk, maar kloppen die argumenten wel? Als we beter kijken naar de feiten, zie je dat hun oplossingen vaak niet werken of zelfs schadelijk zijn.

Immigratie

Wat radicaal-rechts zegt:

“Immigranten pikken onze banen.”

“Ze zorgen voor hogere criminaliteit.”

“Ze kosten alleen maar geld.”

Waarom dit niet klopt:

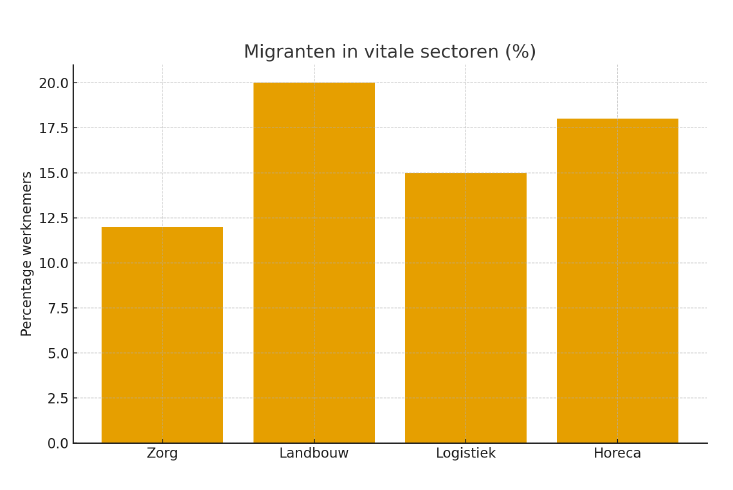

Veel sectoren in Nederland draaien juist op arbeidsmigranten: land- en tuinbouw, logistiek, zorg en horeca. Zonder hen zouden supermarkten leger zijn en prijzen hoger.

Onderzoeken van het CBS laten zien dat immigranten gemiddeld niet meer criminaliteit plegen dan Nederlanders. Bij sommige groepen is de oververtegenwoordiging vooral te verklaren door armoede, niet afkomst.

Immigranten betalen ook belasting en premies. Vooral hoogopgeleide migranten leveren economisch juist winst op.

Kortom: immigratie brengt uitdagingen, maar zonder migranten zou de Nederlandse economie piepen en kraken.

Asiel

Wat radicaal-rechts zegt:

“De asielinstroom is onhoudbaar.”

“Statushouders zorgen voor woningnood.”

“We moeten de Spreidingswet schrappen.”

Wat de feiten zijn:

Asiel en immigratie zijn niet hetzelfde.

Immigratie gaat over alle mensen die naar Nederland komen: voor werk, studie, gezinshereniging, óf asiel.

Asielzoekers zijn mensen die vluchten voor oorlog of vervolging en bescherming vragen op basis van het Vluchtelingenverdrag. Slechts een deel van de totale migratie is dus asiel.

Instroomcijfers (CBS/IND):

2021: ± 36.000 eerste asielaanvragen.

2022: ± 47.000 (mede door de oorlog in Oekraïne).

2023: ± 38.000.

2024: ± 32.000.

De meerderheid van de aanvragen in 2024 was afkomstig uit Syrië.

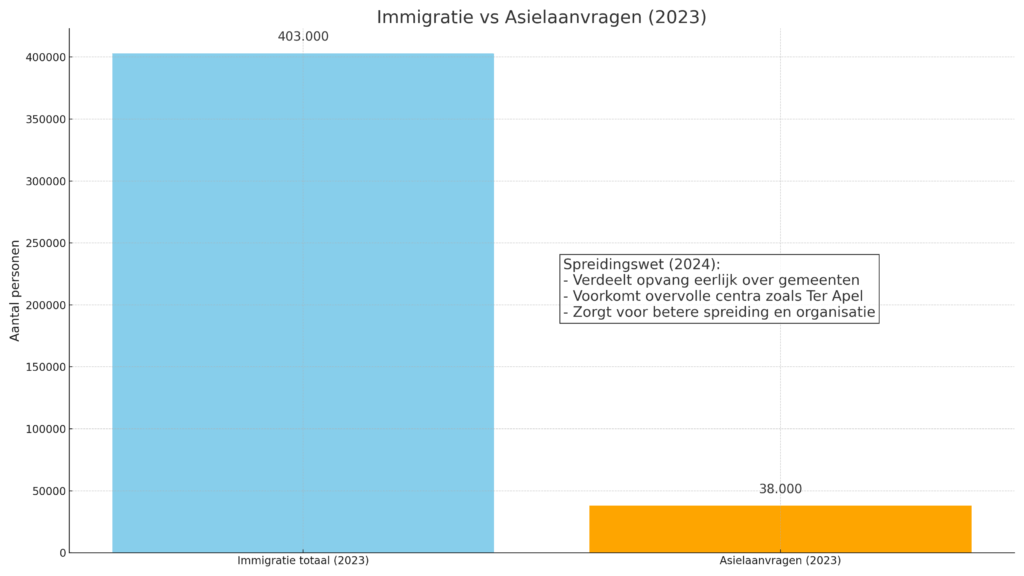

Ter vergelijking: de totale immigratie (alle redenen samen) was in 2023 ruim 403.000 mensen. Dat betekent dat asielzoekers maar een klein deel vormen van de totale instroom.

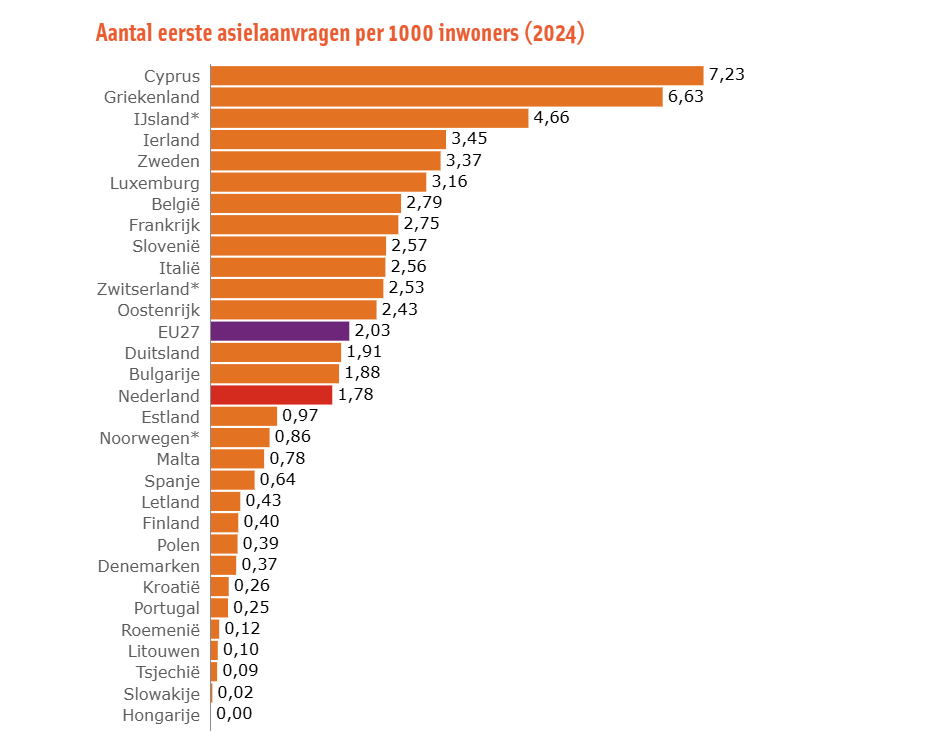

De meeste asielaanvragen in de EU worden in Duitsland gedaan. In 2024 waren dit er 229.750 (25% van het totaal). Daarna volgt Spanje met 164.035 aanvragen en Italië met 15.1120 aanvragen. Samen met Frankrijk en Griekenland vormen zij 82% van het totaal aantal asielaanvragen in de EU.

Hoeveel asielaanvragen krijgt Nederland vergeleken met Europa?

Nederland staat op een zevende plaats met 32.175 aanvragen, achter Duitsland, Spanje, Italië, Frankrijk, Griekenland en België. Je kunt ook kijken naar hoeveel asielverzoeken elk land ontvangt per 1.000 inwoners. Dan staat Nederland op de vijftiende plek. Dat is onder het Europese gemiddelde.

Spreidingswet (2024):

Deze wet zorgt ervoor dat alle gemeenten bijdragen aan opvang van asielzoekers, zodat niet een paar gemeenten of dorpen alles moeten dragen. Dit maakt de opvang eerlijker en beter georganiseerd.

Waarom de angst niet klopt:

De aantallen zijn hoog vergeleken met tien jaar geleden, maar nog steeds beheersbaar in verhouding tot de totale bevolking (±17,9 miljoen).

Nederland vangt relatief (per 1000 inwoners) minder asielzoekers op dan het Europese gemiddelde.

De Spreidingswet zorgt juist voor rust, omdat het voorkomt dat opvangcentra overvol raken en er tentenkampen ontstaan, zoals in Ter Apel.

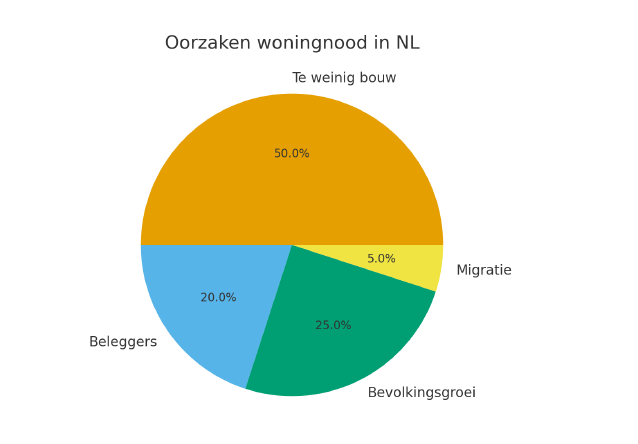

Woningmarkt

Wat radicaal-rechts zegt:

“De woningnood komt door asielzoekers en statushouders.”

Waarom dit niet klopt:

De woningnood is vooral ontstaan doordat er te weinig is gebouwd na de financiële crisis van 2008 en doordat de bevolking groeit.

Slechts 1 op de 30 nieuwe huurwoningen gaat naar statushouders. Het grootste deel wordt verhuurd aan Nederlanders.

Ook beleggers en dure nieuwbouw zorgen voor tekorten: huizen zijn vaak te duur voor starters.

De oplossing ligt dus bij sneller bouwen, betaalbare woningen maken en strengere regels voor beleggers – niet bij het sluiten van grenzen.

Klimaat

Wat radicaal-rechts zegt:

“Klimaatverandering bestaat niet, of is niet door de mens veroorzaakt.”

“Nederland hoeft niets te doen, wij zijn maar een klein land.”

Waarom dit niet klopt:

Wetenschappers zijn het wereldwijd eens: de aarde warmt op door broeikasgassen uit industrie, verkeer en landbouw. Dit is keihard bewezen met data.

Nederland is klein, maar rijk en een grote uitstoter per hoofd van de bevolking. We hebben dus een verantwoordelijkheid.

Bovendien: investeren in duurzame energie maakt ons minder afhankelijk van olie en gas uit landen als Rusland. Dat is ook veiliger en goedkoper op de lange termijn.

Dus: klimaatbeleid is geen hobby, maar noodzaak voor economie, veiligheid en toekomst.

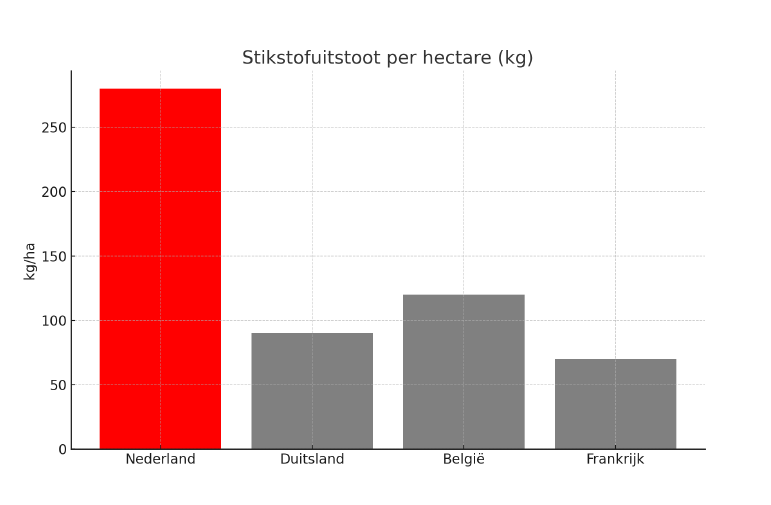

Stikstof

Wat radicaal-rechts zegt:

“Stikstofregels zijn overdreven, boeren moeten gewoon hun werk doen.”

Waarom dit niet klopt:

Nederland is het land met de hoogste stikstofuitstoot per hectare in Europa. Daardoor sterven natuurgebieden, verdwijnen planten en dieren, en komt onze gezondheid in gevaar.

Zonder beperking van stikstof stagneert de bouw. Dat betekent: nog minder huizen, nog minder infrastructuur.

Veel boeren willen zelf verduurzamen, maar hebben duidelijk beleid nodig.

De keuze is dus niet “boeren of natuur”, maar samen naar een gezonde balans.

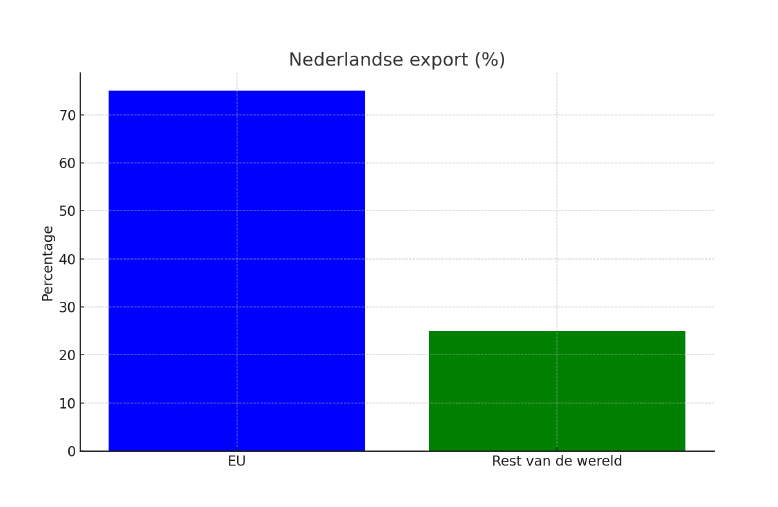

Europese Unie

Wat radicaal-rechts zegt:

“De EU kost ons alleen maar geld.”

“We moeten terug naar de gulden en onze grenzen dichtgooien.”

Waarom dit niet klopt:

Voor elke euro die Nederland inlegt, komt er ongeveer €1,70 terug via handel en subsidies. De EU is onze grootste afzetmarkt: bijna 75% van onze export gaat naar EU-landen.

Zonder EU zou Nederland veel armer zijn: banen in haven, landbouw en industrie hangen direct samen met open grenzen.

Terug naar de gulden zou leiden tot hogere rentes, lagere koopkracht en minder vertrouwen in Nederland.

De EU is dus niet perfect, maar voor Nederland is samenwerken economisch en geopolitiek veel slimmer dan alleen gaan.

Economie

Wat radicaal-rechts zegt:

“Belastingen omlaag, dan wordt iedereen rijker.”

“Minder regels voor bedrijven zorgt voor groei.”

Waarom dit niet klopt:

Lagere belastingen klinken leuk, maar betekenen ook minder geld voor zorg, onderwijs en veiligheid. Uiteindelijk betaalt de gewone Nederlander de prijs.

Te weinig regels leiden vaak tot misbruik en ongelijkheid. Denk aan de bankencrisis in 2008: te weinig toezicht veroorzaakte miljarden schade.

Investeren in onderwijs, innovatie en duurzaamheid levert juist economische groei én banen op.

Conclusie

Radicaal-rechtse partijen bieden simpele antwoorden op moeilijke problemen. Maar echte oplossingen zijn nooit zo zwart-wit. Immigratie, klimaat, wonen en economie vragen om samenwerking, slimme investeringen en eerlijk beleid – niet om muren, haat of ontkenning van feiten.

Wie verder kijkt dan de korte leus, ziet dat de argumenten van radicaal-rechts vooral op emoties spelen en vaak niet kloppen. Feiten en toekomstgericht beleid brengen ons wél vooruit.

September 2025 inflation in the Netherlands came in at 3.3%, significantly higher than the eurozone average of 2.2%. While many households experience this simply as “prices rising again,” the underlying dynamics are more structural than temporary — and that matters for wages, pensions, and policy.

Why Dutch Inflation Is Consistently Higher

Economists have long noted that Dutch prices rise faster than those of their neighbors. Since the introduction of the euro in 2002, inflation in the Netherlands has run systematically above the eurozone average. Several factors explain this:

Tight labor market – The Netherlands has one of the lowest unemployment rates in Europe. With labor scarce, wages rise faster, and businesses pass on those costs.

Service-heavy economy – A large share of the Dutch economy is service-based, where labor costs are the dominant factor. Wage increases feed more directly into consumer prices than in Germany’s industry-heavy economy.

Tax and regulatory effects – Changes in VAT, energy taxes, and housing policies have historically added volatility and upward pressure compared to countries with more stable regimes.

The result: a structural inflation premium compared to their European peers.

September 2025: A Perfect Storm

The September figures highlight three simultaneous drivers:

Fuel & energy – About half of the increase stems from higher oil and energy prices. This is highly volatile but immediately visible to consumers at the pump and on utility bills.

Wages – Dutch wages have risen sharply in 2024–2025 as unions fought to protect purchasing power. This creates a feedback loop: higher prices → higher wage demands → higher prices.

Eurozone effect – While inflation rose in Europe overall (from 2.0% to 2.2%), the Dutch figure of 3.3% underscores the widening gap: 0.8 percentage points above the average, double the divergence of a month earlier.

Implications for Policy and Consumers

European Central Bank (ECB) – With inflation ticking up across the eurozone, rate cuts are off the table. For the Netherlands, this means tighter credit conditions even though our inflation problem is wage- and structure-driven, not monetary.

Purchasing power – For households, the outlook is grim. Real wage gains are limited because wage hikes feed inflation themselves. Pensioners, tied to indexation rules, also risk losing ground if inflation stays above assumptions.

Competitiveness – Dutch goods and services risk becoming more expensive relative to neighboring markets. This could push consumers to shop across borders (as seen in supermarket price comparisons) and pressure export margins.

Outlook: Here to Stay

Projections from Rabobank and the CPB (Dutch Central Planning Bureau) suggest inflation will average 3.2–3.3% in 2025 and only decline to around 2.4% in 2026. That remains well above the ECB’s 2% target.

The concern is not just the short-term squeeze at the gas pump, but a long-term erosion of purchasing power. Over 25 years, consistently higher inflation means Dutch consumers lose significantly more ground than their German, Belgian, or French counterparts — with ripple effects on pensions, savings, and confidence in economic policy.

Key Takeaway

Dutch inflation is not just about temporary oil shocks. It is structural, linked to the Dutch labor market and service-based economy. As long as wage growth translates directly into price growth, the Netherlands will continue to outpace the eurozone in inflation — and consumers will feel it in their wallets.

Parliamentary elections will be held in the Netherlands on October 29. A key question is how much influence the inflation figures will have on the outcome.

Heatwaves, droughts, and floods that struck Europe over the past summer caused an estimated €43 billion in immediate economic losses, according to a new study by the University of Mannheim in collaboration with economists from the European Central Bank.

The researchers looked at the true cost of climate change in a broad sense: not only the direct and tangible destruction of homes and crops, but also indirect effects such as disruptions to rail transport and reduced labor productivity during extreme heat. Using meteorological data and economic modeling, they calculated that the macro-economic costs could rise to €126 billion by 2029.

The authors stress that their estimates are “conservative,” since several major events—such as the record-breaking wildfires in Southern Europe last month—were not included in the analysis.

Unequal Impact Across Europe

The damage is not evenly distributed. Low-income regions and those with higher temperatures are hit the hardest. Spain, France, and Italy, which faced prolonged heatwaves and drought, each recorded losses exceeding €10 billion this year alone. In the medium term, these costs could rise beyond €30 billion per country.

Central and Northern Europe saw less immediate damage, but floods are becoming increasingly common there as well, suggesting that the costs of climate change will continue to mount across the continent.

Long-Term Consequences

The study also highlights the long-term drag on productivity. Four years after a drought, a region’s GDP is on average 3 percentage points lower than before. In the case of flooding, GDP remains 2.8 percentage points lower.

These findings underscore how climate extremes are not only an environmental challenge but also a profound economic threat—one that will shape Europe’s future growth and resilience in the years to come.

Based on President Trump’s public statements about the EU-US trade deal announced on 27 July 2025, here’s how they align or potentially contradict the European Commission’s framing:

Points of Agreement

Both sides emphasize:

The 15% tariff ceiling: Trump confirmed that the U.S. will impose a flat 15% tariff on most EU goods, including cars, which is consistent with the EU’s statement.

Energy and investment commitments: Trump highlighted the EU’s agreement to purchase $750 billion in U.S. energy and invest $600 billion in the U.S., which matches the EU’s announcement.

Strategic product exemptions: Both sides noted that certain products like aircraft parts,chemicals, and pharmaceuticals will receive special treatment or exemptions.

Section 232 investigations: Trump acknowledged that pharmaceuticals and semiconductors will temporarily face 0% tariffspending national security reviews, aligning with the EU’s description.

Here’s where Trump’s tone or framing may differ from the EU’s:

Tariff Framing:

Trump described the deal as a “very powerful” and “biggest of all the deals”, emphasizing tough negotiations and portraying the 15% tariff as a win for the U.S.

EU framing presents the 15% as a ceiling that reduces existing tariffs (e.g., on cars from 25% + 2.5% MFN), suggesting relief rather than escalation.

EU Expectations:

Reports indicate that Europe had hoped for lower tariffs, around 10%, and some EU officials expressed relief mixed with concern over the final deal.

Trump’s tone suggests the EU market was “essentially closed” and now “opened up,” which may not reflect the EU’s view of its own openness.

Military Purchases:

Trump mentioned that the EU would be “purchasing hundreds of billions of dollars worth of military equipment”, a claim not mentioned in the EU’s official statement.

Steel and Aluminum Tariffs:

Trump indicated that 50% tariffs remain for now, with a quota system to be negotiated. The EU emphasized cutting tariffs and protecting against global overcapacity, suggesting a more cooperative tone.

Moreover: the EU-US trade deal announced on 27 July 2025 is a political agreement and not legally binding until it is formally ratified through the EU’s internal procedures, which may require approval from all 27 member states.

What defines a strong NATO ally? Since the alliance’s founding in 1949, debates over burden-sharing have been constant. Donald Trump, both in his first and current term, has sharply criticized European members for underfunding their defense while relying on U.S. protection—and not without reason.

His message is resonating. Belgium’s defense minister recently vowed to end the country’s “national shame” of being NATO’s most notorious free rider. Even Iceland, which lacks a standing army, is exploring how to contribute more meaningfully.

Image: Pixabay

To assess NATO members’ contributions, consider the “three Cs”: cash, capabilities, and commitment.

Cash: More Members Are Meeting Targets—But Is It Enough?

Today, 22 of NATO’s 32 members meet the 2% of GDP defense spending target, a big jump from just seven a decade ago. Italy and Spain are on track to join them this year. But the bar is rising: at the upcoming summit in The Hague, NATO is expected to adopt a new target of 3.5% of GDP, plus 1.5% for supporting infrastructure.

Still, raw spending figures can be misleading. Some countries inflate their numbers by including loosely related expenses under “defense.”

Capabilities: What the Money Buys Matters More

NATO recommends that at least 20% of defense budgets go toward equipment—most members comply, and that threshold may soon rise to 33%. But quantity doesn’t equal quality. Greece, for example, spends heavily on gear, but much of it is aimed at deterring Turkey, not Russia.

The NATO Defense Planning Process aims to align national purchases with alliance needs. After years of counterterrorism focus, the threat from Russia is refocusing priorities. Allies are now being asked to build forces primarily for deterrence in Europe. New “capability targets” expected this month will guide what each country should provide—especially in areas where the U.S. may scale back, like intelligence, long-range strike, and logistics.

Commitment: Who Shows Up?

Operationally, even the most frugal allies are stepping up. Spain leads a multinational brigade in Slovakia; Italy commands one in Bulgaria. Portuguese jets patrol Baltic airspace. Smaller nations like Albania and Slovenia also contribute troops to NATO’s eastern flank.

But NATO wants more. In a major conflict, it aims to deploy 100,000 troops within 10 days and another 200,000 within 30. Without more European investment in recruitment and readiness, those goals may be out of reach—especially without U.S. troops.

A Smarter Division of Labor?

NATO is exploring a “multi-speed” model: larger militaries take on high-end combat roles, while smaller states focus on logistics, cyber, or niche capabilities. Luxembourg, for instance, supports satellite communications and surveillance; Iceland runs an air-defense system.

Getting underperformers like Spain and Italy to specialize more effectively may be key. Encouraging them to invest in maritime capabilities could be a strategic win.

Manage Cookie Consent

To provide the best experiences, roelthijssen.nl uses technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.